How to find and vet qualified buyers when selling your insurance agency

When the time comes for selling your insurance agency, finding the right buyer is perhaps the most consequential decision you’ll make. The wrong buyer—even one who pays cash—can destroy the legacy you’ve built, alienate your clients, and mistreat your staff. The right buyer preserves what matters while delivering fair value for your life’s work.

This guide walks you through everything you need to know to identify, approach, and thoroughly vet potential acquirers. Whether you’re considering a sale next year or five years from now, understanding the buyer landscape will help you make smarter decisions when the time comes.

Where to find qualified buyers

Finding qualified buyers requires a multi-channel approach because different buyer types hunt for agencies through different channels. You can’t simply post on one website and expect to receive serious offers.

Your Immediate Network. Start with other agency owners you know who’ve expressed interest in growth. These conversations take place at industry conferences, through local associations, and through carrier relationships. Some of the best deals come from relationships built over years, not from cold outreach. An owner in your market who knows your reputation, understands your client base, and has observed your agency’s operations will often pay premium multiples because they’re buying certainty, not just financials.

Active Acquirers. The Insurance Journal’s Top 100 list is a goldmine for identifying agencies that grow through acquisition. These organizations didn’t become large by accident—they grew through strategic acquisitions, and most are constantly looking for their next deal. Research which ones operate in your region or are expanding into it. Don’t send your CIM blindly; study their acquisition history, understand what they’re looking for, and craft personalized outreach that explains why your agency fits their strategy.

Business Brokers. Specialized insurance agency brokers have buyer databases you can’t access independently. They know who’s actively looking, who has financing lined up, and who’s serious versus tire-kicking. The trade-off is paying a 6-10% commission, but a good broker screens buyers, manages negotiations, and often secures better terms than you’d achieve on your own because they understand leverage and deal structure.

Private Equity-Backed Platforms. Firms like Baldwin Risk Partners, Acrisure, Hub International, and dozens of others have raised capital specifically to consolidate insurance agencies. They move fast, pay fairly, and have streamlined processes—but they also have specific criteria about size, geography, and operations.

The real question isn’t “where do I find buyers?” but “how do I find the right buyer?” Casting too wide a net burns time and risks confidentiality. Targeting 15-20 qualified prospects who match your size, geography, and values will produce better results than broadcasting to hundreds.

Real experience: Managing buyer inquiries

“When we decided it was time to start selling our insurance agency, I knew we needed help,” says Deni Townsend, whose agency had been in her family since the 1930s and 1940s—three generations of clients and deep community relationships. “The moment we put the word out, we were absolutely bombarded with inquiries. Everyone wanted financials, loss runs, valuations—the requests were overwhelming. I remember telling my husband Billy, ‘I can’t manage all of this paperwork while still doing my job.”

Deni’s experience illustrates why finding buyers is only half the challenge. Managing buyer inquiries while running your day-to-day operations can quickly become overwhelming without the right support structure in place.

How to verify a buyer’s financial capability

Nothing wastes more time than spending 90 days negotiating with a buyer who can’t actually secure financing. Vetting financial capability upfront saves you months of wasted effort and prevents the emotional letdown of a deal that falls through.

Ask direct questions early—during the second or third conversation, not during final negotiations. “How are you planning to finance this acquisition?” is a completely reasonable question. Serious buyers expect it and have clear answers. Buyers who get defensive or evasive about financing raise immediate red flags.

All-Cash Buyers (private equity platforms, large agencies, well-capitalized independents) are most reliable because financing isn’t contingent. They should provide proof of funds—typically a bank statement or letter from their CFO confirming available capital. Don’t hesitate to request this; it’s standard in transactions of this size.

SBA-Financed Buyers (common among individual entrepreneurs) represent moderate reliability. SBA 7(a) loans can finance up to 90% of the purchase price, but approval takes 60-90 days and requires seller involvement. The buyer should already have preliminary SBA lender approval before making formal offers. Ask: “Have you been prequalified by an SBA lender? What’s your credit score and down payment capability?” Buyers with credit scores under 700 or down payments under 10% rarely close.

Seller-Financed Deals shift risk to you but expand your buyer pool. This works when the buyer has strong industry experience and some capital, but not enough for a full purchase. Structure it carefully with personal guarantees, a first-position security interest, and clear default terms.

Red Flags That Signal Financially Incapable Buyers: They want to tour your agency and meet your staff before proving financing (time-wasters using your process to gather competitive intelligence). They propose complicated equity structures where you take risk but they get control. They’ve been “looking at agencies” for over two years but have never closed a deal. They propose earnouts that put 70% or more of your payment at risk over five years or more.

Before spending serious time with any buyer, get proof of funds or a lender prequalification letter, a personal financial statement (for individual buyers), an explanation of how they’ve structured previous acquisitions, and references from sellers they’ve previously purchased from. A qualified buyer won’t hesitate to provide this information.

Strategic Buyers vs. Financial Buyers: Understanding the Difference

Understanding buyer types helps you evaluate offers that may appear similar on the surface but have significantly different implications for you, your staff, and your clients.

Strategic buyers are other insurance agencies or industry operators acquiring your agency to expand their footprint, add capabilities, or gain scale. They’re buying for operational reasons—accessing your markets, carrier relationships, or expertise. These buyers typically offer 1.8x-2.6x revenue multiples, prefer all-cash or mostly cash structures, and focus on integrating your agency into their operations. Your brand may disappear, your staff might be consolidated, and your office may close. The upside: they understand insurance, move decisively, and can close quickly. If you want a clean exit with minimal ongoing involvement, strategic buyers often deliver that.

Financial buyers are private equity firms, family offices, or investment funds that buy agencies purely for financial returns. They’re less common among small agencies (most want $2M+ in revenue), but they’re increasingly active. They typically offer 2.3x-3.0x+ revenue but structure deals with significant earnouts tied to performance, retention, and growth targets. The upside: higher potential total compensation if earnout targets are hit. They usually keep your brand, retain your staff, and want you involved for 2-5 years post-sale. The downside: your payout is heavily contingent on future performance, and you no longer have complete control.

Which is better? It depends on your priorities. If you’re 65, want to retire, and value certainty, a strategic buyer paying 2.2x cash is preferable to a financial buyer offering 2.8x with 60% in earnouts over four years. If you’re 55, energetic, and confident in continued growth, the financial buyer might deliver more total compensation. Evaluate offers based on total cash at closing (not theoretical earnout maximums), achievability of earnouts, your required post-sale involvement, and what happens to your staff and clients.

Should you consider selling to an employee?

Employee sales can be phenomenal or disastrous, and the difference usually comes down to three factors: the employee’s capability to actually run the business, their financial capacity to buy it, and whether you can emotionally handle the transition dynamic.

The case for employee sales: Your key employee already knows the clients, understands the operations, and has relationships with carriers. Transition risk is minimal. Clients often respond positively because they already trust this person. Your legacy is more likely to be preserved.

The capability question: Being a great account manager doesn’t automatically translate to being a successful agency owner. Does this employee understand P&L management? Can they handle sales and business development? Do they have leadership skills? Most critically — are they willing to work the hours and take the risks that ownership demands?

The financial reality: Most employees can’t write a check for your agency. They’ll need SBA financing, which means you’ll likely carry a seller note of 10-20% of the purchase price. Structure it carefully, including personal guarantees, life insurance requirements, and performance covenants to protect your note.

Here’s how to evaluate whether an employee sale makes sense: Give them increasing ownership responsibility 12-24 months before a potential sale. Let them run the agency for 2-3 months while you’re minimally involved—do they thrive or struggle? Have frank financial conversations early. And critically, obtain an outside valuation and negotiate at arm’s length—don’t discount your price by 30% just because you like them.

Maintaining confidentiality while marketing your insurance agency

Confidentiality failures erode agency value more quickly than almost anything else. Word leaks that you’re selling, clients panic and start shopping, employees get nervous and update their resumes, competitors spread rumors, and your revenue can drop 10-20% before you even have a buyer.

Start with a marketing teaser—a one-page, anonymous overview of your agency that includes key metrics but no identifying information. Include revenue, growth rates, client concentration, and geographic region, but not your agency name, specific location, or carrier breakdown that would identify you. This teaser gauges interest before revealing your identity.

Require NDAs (Non-Disclosure Agreements) before sharing your Confidential Information Memorandum. The NDA should prohibit disclosing receipt of information about your agency, contacting your clients or employees, soliciting your staff, and using information for competitive purposes.

Limit initial distribution. Don’t blast your confidential information memorandum (CIM) to 50 potential buyers. Target 10-15 highly qualified prospects who match your profile. Use a secure virtual data room for due diligence documents, not Dropbox or email. Conduct meetings off-site, never at your agency during business hours. Never use identifiable client names in initial materials.

Real experience: The complexity of finding the right buyer

Ken Pickett faced a unique challenge when selling an insurance agency that had been in his family for over 42 years. “I had real concerns about doing this the right way,” Ken explains. “I wanted to make sure my customers were taken care of, my full-time employees landed somewhere good, and that the agency stayed together rather than being split apart.”

Ken’s biggest challenge was one many sellers don’t anticipate: “The biggest challenge was that I had absolutely no idea how to transfer the 25-35 different insurance companies we were doing business with. Transferring all these independent company appointments was a deal-breaker for me—they had to go to the new owner, or we didn’t have a deal.”

With professional guidance, Ken found a buyer who could truly benefit from what his family had built, met his hard deadline, and moved on to the next phase of his life with confidence.

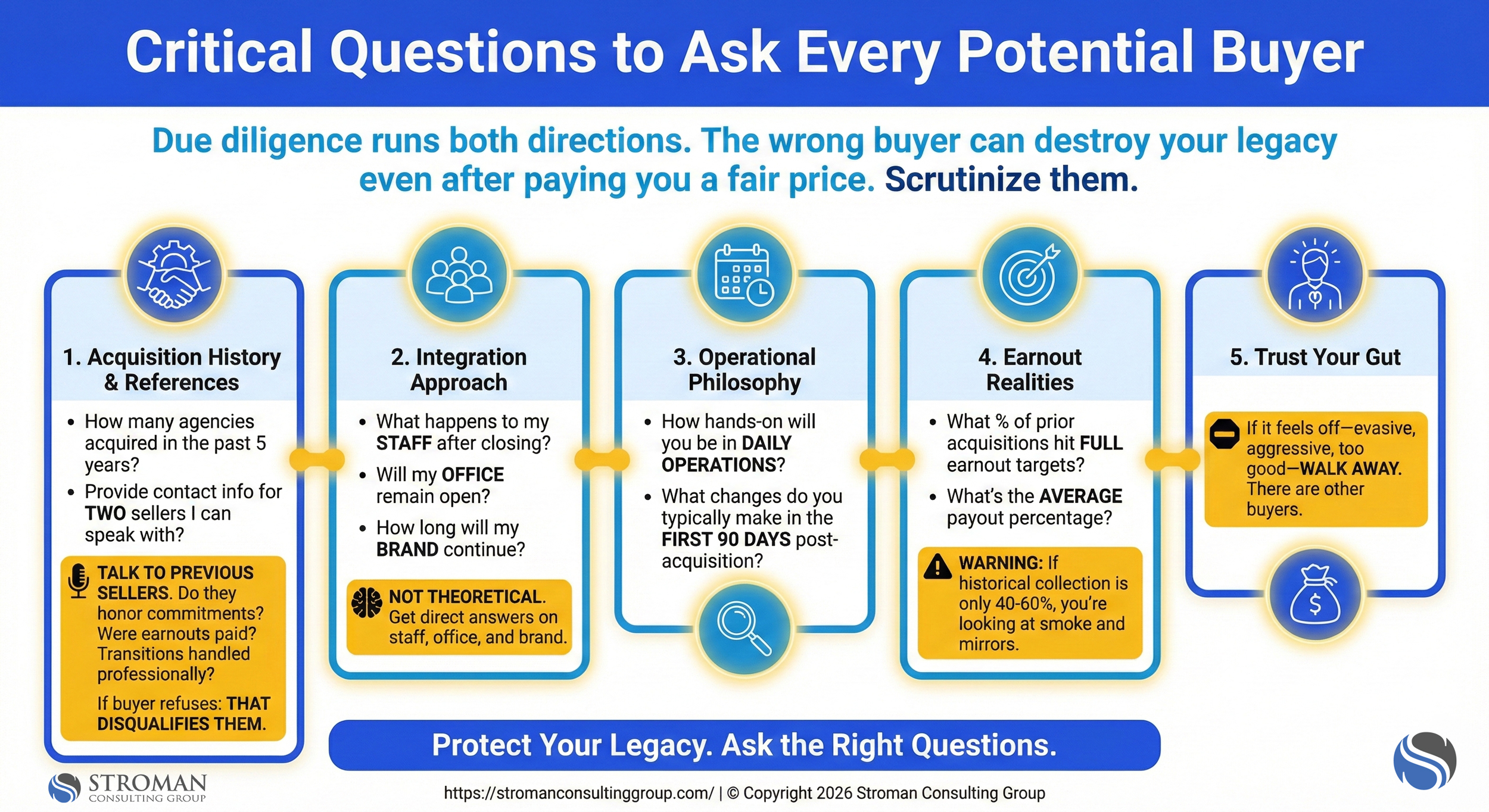

Critical questions to ask every potential buyer

Due diligence runs both directions. While buyers scrutinize your agency, you should scrutinize them as well. The wrong buyer can destroy your legacy even after paying you a fair price.

Ask about their acquisition history: “How many agencies have you acquired in the past five years? Can you provide contact information for two sellers I can speak with?” Talking to previous sellers reveals how buyers actually behave after closing. Do they honor commitments? Did earnouts get paid? Were transitions handled professionally? If a buyer refuses to provide seller references, that disqualifies them.

Understand their integration approach: “What happens to my staff after closing? Will my office remain open? How long will my brand continue?” These aren’t theoretical questions—they have direct answers.

Explore their operational philosophy: “How hands-on will you be in daily operations? What changes do you typically make in the first 90 days post-acquisition?”

Ask about earnouts specifically: “What percentage of your prior acquisitions have hit full earnout targets? What’s the average payout percentage?” If sellers historically only collect 40-60% of projected payments, you’re looking at smoke and mirrors.

Finally, trust your gut. You’ve developed business instincts over decades. If something feels off about a buyer—they’re evasive, overly aggressive, or make promises that sound too good—walk away. There are other buyers.

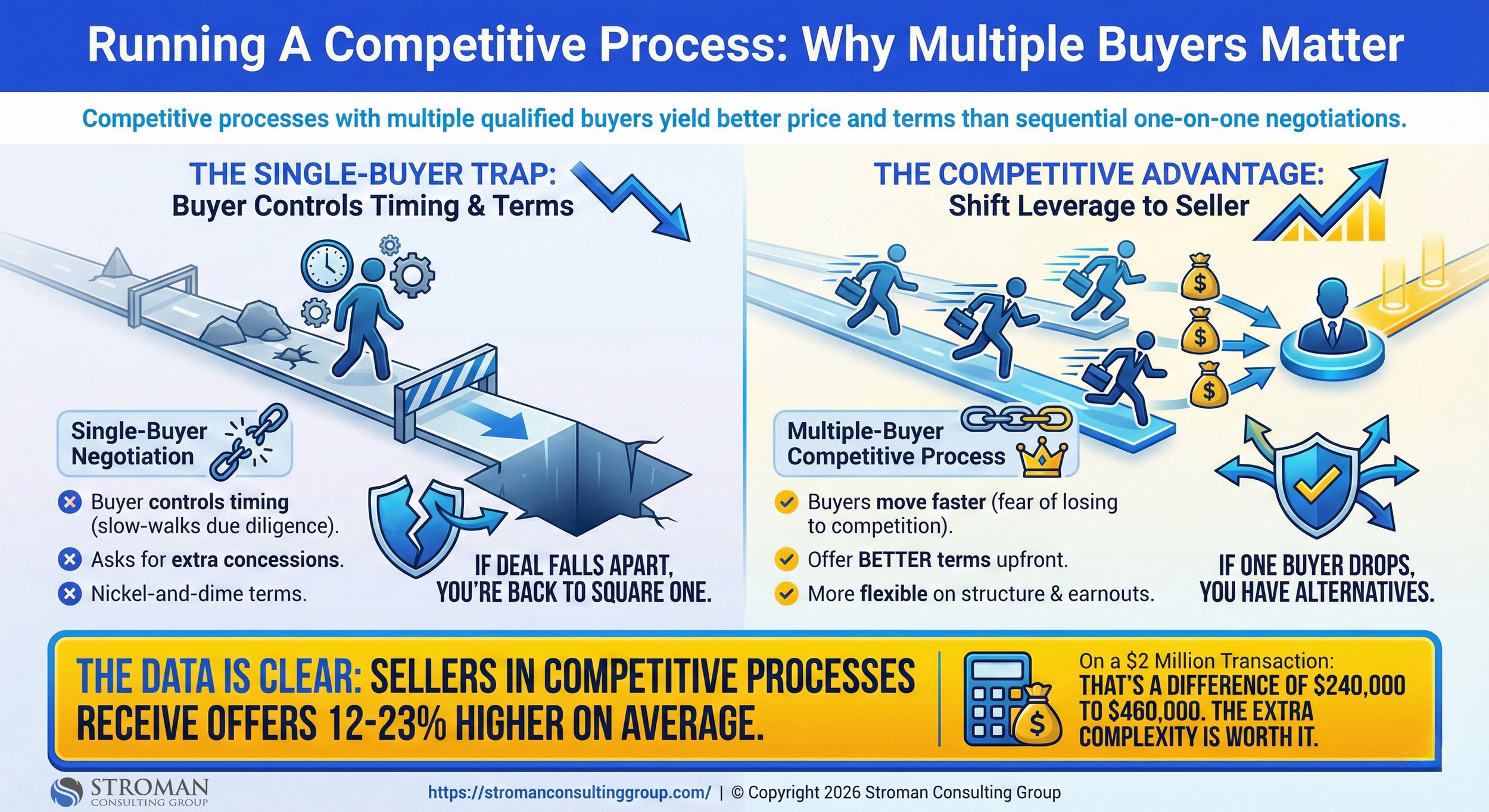

Running a competitive process: Why multiple buyers matter

Running a competitive process with multiple qualified buyers simultaneously is almost always preferable to sequential one-on-one negotiations, both in price and terms.

With single-buyer negotiations, they control timing. They know you’re not entertaining other offers, so they can slow-walk due diligence, ask for extra concessions, and nickel-and-dime terms. If the deal falls apart, you’re back to square one.

Multiple-buyer dynamics shift leverage entirely. Buyers move faster because they fear losing to competition. They offer better terms upfront. They become more flexible on structure and earnouts. Most importantly, if one buyer develops cold feet, you have alternatives.

The data is clear: sellers who run competitive processes receive offers 12-23% higher on average than those who negotiate with single buyers. On a $2 million transaction, that difference is $240,000 to $460,000. The extra complexity is worth it.

Should you rule out consolidating buyers?

A buyer who already owns an agency in your market and plans to consolidate creates obvious considerations. Your office probably closes. Your staff likely become redundant. Your brand disappears. Everything you built gets absorbed.

If preserving your legacy, protecting staff jobs, and maintaining your brand matter significantly, a consolidating buyer probably isn’t the right fit—regardless of their offer. However, the financial case for consolidating buyers is strong: they often pay premium multiples because they achieve immediate cost synergies. An offer of 2.6x from a consolidating buyer might be better than 2.2x from a buyer keeping your agency standalone.

The middle ground: negotiate retention protections into the purchase agreement. Require that all staff be offered comparable positions for at least 12 months. Negotiate a retention bonus pool. Include provisions that key employees terminated without cause within 18 months trigger additional payments to you.

Getting expert help with your Insurance Agency sale

The process of selling an insurance agency involves dozens of moving pieces: identifying qualified buyers, vetting their financial capability, managing confidentiality, negotiating terms, handling carrier transfers, and ensuring your clients and employees are protected throughout the transition.

As Deni Townsend reflects on her experience: “Mike understood both the emotional and business sides of selling an insurance agency. This wasn’t just a transaction for us—we cared deeply about our employees and our clients being taken care of. Mike put everything in perspective and made sure our priorities were protected. Four years later, I’m fully retired (as planned!), and everything worked out exactly as we hoped.”

Whether you’re planning to sell next year or simply want to understand your options, having the right guidance makes all the difference. Download our comprehensive roadmap at stromanconsultinggroup.com for detailed guidance on buyer types, red flags to avoid, and negotiation strategies that protect what you’ve built.