HOW TO SELL YOUR INSURANCE AGENCY

Utilize The Mike Stroman How to Sell Your Insurance Agency Road Map to navigate the steps for selling your independent insurance agency.

Click on the explore icons

throughout the map to get Mike Stroman’s personal advice on the topics.

CONTENT

Gathering Critical Data for Selling an Independent Insurance Agency

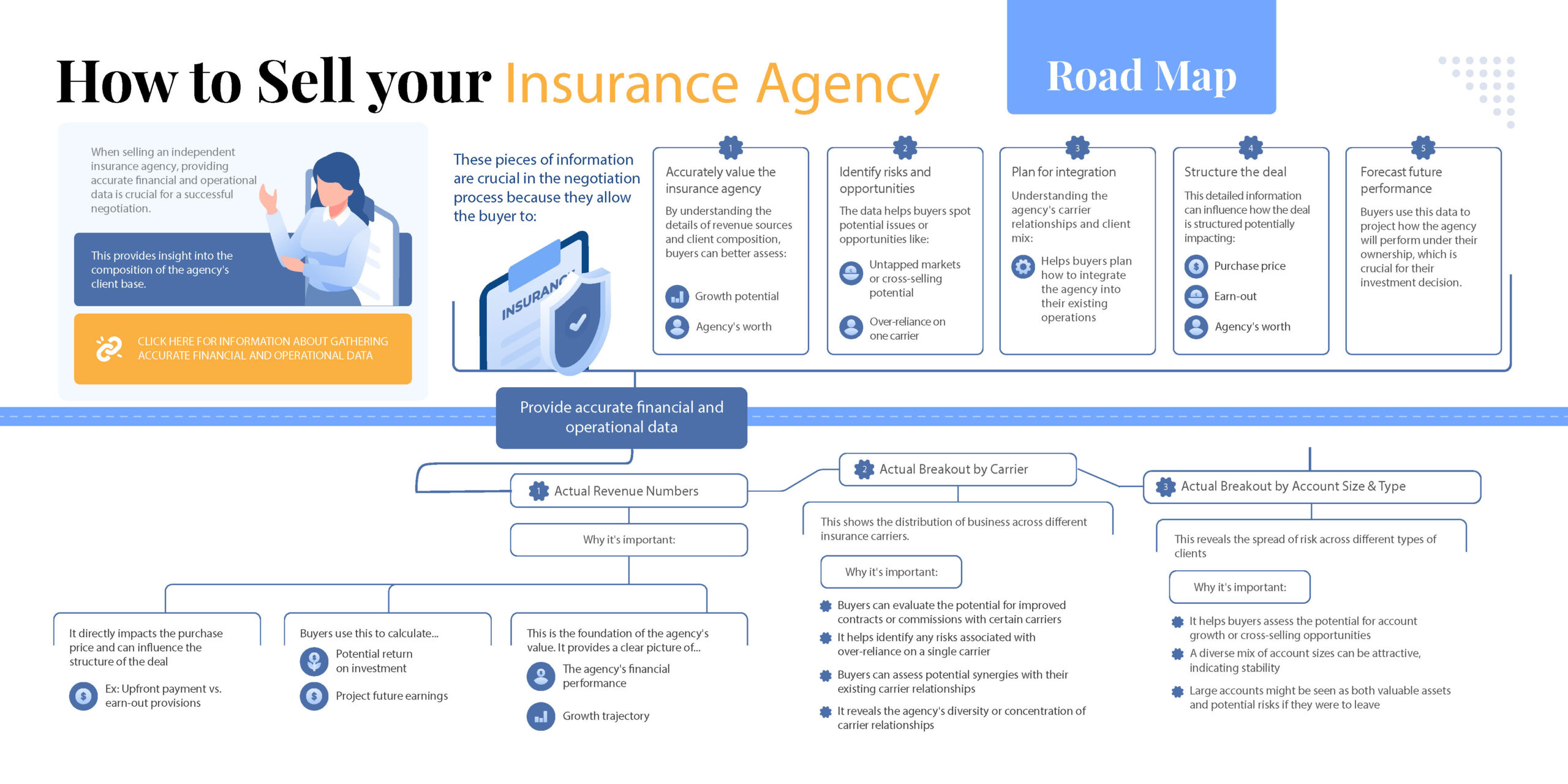

When selling an independent insurance agency, providing comprehensive and accurate financial and operational data is crucial for a successful negotiation. Three key components of this data are actual revenue numbers, carrier breakouts, and account size breakouts.

This information forms the foundation for valuing the insurance agency and helps potential buyers understand its operational structure and growth potential.

Data Collection Process

The process of gathering this vital information typically involves leveraging the agency’s management system and financial records. Most agencies utilize Agency Management software such as Applied Epic, Vertafore AMS360 or Hawksoft that tracks policies, premiums, and commissions and hopefully integrate agency revenue with accounts.

Revenue numbers are usually extracted from accounting software and financial statements, which should be perfectly aligned. If one of these systems is not in sync with the other, stop the presses and find the problem. Inaccuracies are death in the Data Collection Process.

Carrier breakouts can usually be obtained on an annual, quarterly or monthly basis directly from your insurance carriers and wholesale brokers. If they can be downloaded in a report format and Excel format – get both. We can display your information in a much more compelling view via Excel, but Buyers will always also want the actual carrier reports with the carrier’s agency code displayed for validation.

Account size breakouts require a more detailed analysis of the client database, possibly involving custom reports involving several carriers. Always give the last 3 years of premium and commission for each large account. In addition to the raw data, it is also critical to know how long you’ve had the account, and if they are in a growth mode.

Given the importance of accuracy, many sellers engage consultants such as myself (Stroman Consulting Group) to assist in compiling and verifying this information.

Importance in Negotiations

Each piece of this data plays a crucial role in the negotiation process. Actual revenue numbers form the foundation of the agency’s valuation, providing a clear picture of financial performance and growth trajectory. This directly impacts the purchase price and can influence the deal structure.

The breakout by carrier reveals the distribution of business across different insurance carriers, highlighting the agency’s diversity or concentration of relationships. This information allows buyers to assess potential synergies with their existing carrier relationships and identify any risks associated with over-reliance on a single carrier.

The breakout by account size offers insight into the composition of the agency’s client base, showing the spread of risk across different types of clients and indicating stability or growth potential.

Impact on Buyer’s Decision-Making

This detailed information enables potential buyers to accurately value the agency, identify risks and opportunities, plan for integration, structure the deal appropriately, and forecast future performance. It allows buyers to project how the agency might perform under their ownership, which is crucial for their investment decision. Providing this level of detail not only demonstrates transparency and professionalism but also allows for more informed negotiations, potentially leading to a better outcome for both parties.

If you’re working with Stroman Consulting Group, it also allows us to present the information in the most favorable light.

Broader Considerations

While this financial and operational data is crucial, it’s important to remember that other factors like agency culture, staff capabilities, and market position also play significant roles in the overall valuation and attractiveness of an agency to potential buyers. Furthermore, proper confidentiality agreements should be in place before sharing such sensitive information.

By providing comprehensive, accurate data on revenue, carrier relationships, and account sizes, sellers can facilitate a more effective and potentially more profitable negotiation process while buyers can make more informed decisions about the potential acquisition.

CONTENT

The most important considerations when selling an insurance agency and why they matter

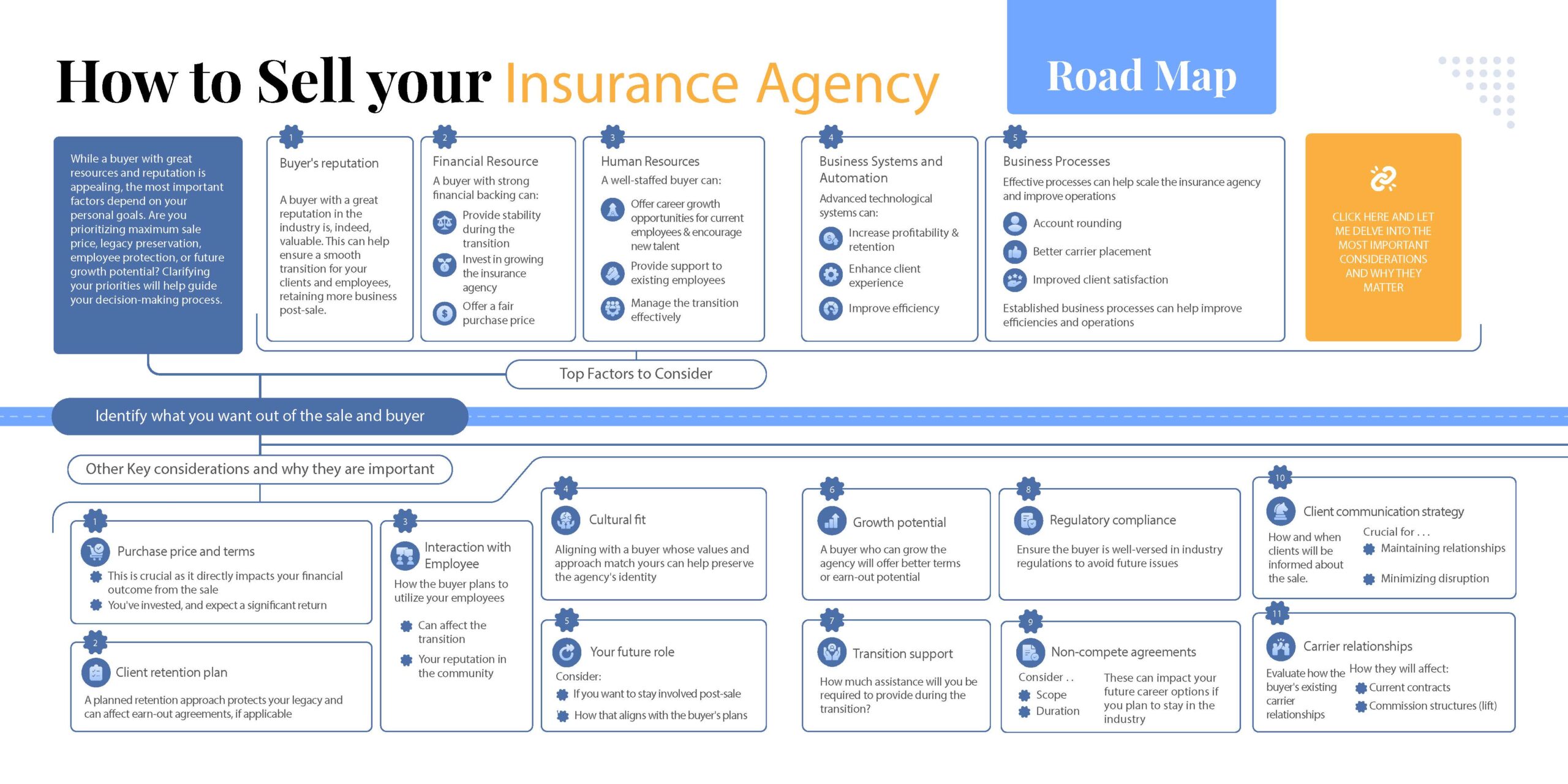

When selling an independent insurance agency, a buyer with an excellent reputation, substantial resources, advanced systems, and robust business processes can indeed be very attractive. However, weighing multiple factors is essential to ensure the best outcome for you, your clients, and your employees.

Let’s explore the most important considerations and why they matter:

While a buyer with the qualities we’ve described can offer significant advantages, it’s essential to evaluate each potential buyer holistically. The ideal buyer will offer a balance of these factors that aligns with your priorities and goals for the sale. Remember, the best choice isn’t always the highest bidder or the largest company but the one that offers the best overall fit for your agency’s future and your personal objectives.

CONTENT

How would I prioritize these key considerations in your decision-making process?

The first step in prioritizing your decision-making process is to clearly define your primary goals for the sale. Take some time to reflect on what matters most to you – whether it’s maximizing your financial return, ensuring the welfare of your clients and employees, preserving your agency’s legacy, facilitating future growth, planning for your life after the sale or a combination of all of these factors. These core objectives will serve as the foundation for your entire decision-making process.

Weighted-Scoring System

Once you’ve established your goals, consider creating a weighted scoring system. This approach allows you to assign relative importance to different factors based on how they align with your objectives. For instance, you might decide that financial considerations should carry the most weight, followed closely by client retention and service quality, then employee welfare, agency growth potential, and finally, personal factors such as non-compete agreements or your future role.

With your weighted system in place, you can begin to evaluate each consideration more objectively. Rate each factor on a consistent scale for every potential buyer. This could involve creating a decision matrix – a spreadsheet where you list all considerations, their weights, and scores for each buyer. This visual tool can be invaluable in comparing options side-by-side and identifying the strengths and weaknesses of each potential buyer.

Deal Breakers

While working through this analytical process, it’s crucial to identify any absolute deal-breakers as well. These are non-negotiable factors that would automatically disqualify a buyer, regardless of their strengths in other areas. Keeping these in mind can help you quickly narrow down your options and focus your energy on the most promising candidates.

Don’t hesitate to seek external input as you work through this process. Consult with financial advisors to understand the tax implications and optimal deal structures. Speak with legal counsel about contracts and regulatory considerations. Reach out to industry experts such as the Stroman Consulting Group, who have gone through similar sales consistently, and learn from their experience. You can also consider getting insights from trusted employees or partners who understand your agency’s day-to-day operations.

Timeline

Remember to align your considerations with your desired timeline for the sale and transition period. Some factors may become more or less important depending on how quickly you want to complete the sale and how involved you plan to be during and after the transition.

Strengths and Weaknesses

Look for synergies between your agency and potential buyers. A buyer whose strengths complement your agency’s weaknesses (or vice versa) could be particularly well-positioned to drive future growth and success.

Successful Sale

While it’s important to be as objective as possible in your analysis, don’t discount the value of your instincts. After you’ve done the analytical work, take some time to consider your gut feeling about each buyer. Factors like cultural fit and personal comfort level are difficult to quantify but can be crucial to a successful sale and transition.

Throughout this process, try to prioritize long-term considerations over short-term gains. While the immediate sale price is undoubtedly essential, factors affecting the agency’s long-term success and your peace of mind may prove more valuable in the long run.

Adjust Your Priorities

Finally, be prepared to revisit and adjust your priorities as you gather more information during the sale process. Selling an agency is a complex endeavor, and new factors may come to light that shift your perspective. Remaining flexible and open to adjusting your approach will help ensure you make the best decision for yourself, your clients, and your employees.

CONTENT

What do sellers of Independent Insurance Agencies generally want?

Sellers of independent insurance agencies typically have a complex set of desires when looking to sell their businesses. While maximizing financial return is often a top priority, many sellers are equally concerned with preserving their legacy and ensuring the continued well-being of their clients and employees.

Sellers generally seek a buyer who can offer a fair valuation while also demonstrating the capability to maintain high-quality client service and provide opportunities for staff growth.

Many sellers hope to see their agency continue to thrive and grow under new ownership, with access to expanded markets or improved technologies.

There’s often a strong desire for a smooth transition process that minimizes disruption to day-to-day operations and maintains the agency’s standing in the community.

Personal considerations also play a significant role, with sellers looking for alignment with their own exit strategies and future plans. This might involve flexibility in their post-sale involvement or ensuring that non-compete agreements are reasonable.

Ultimately, most sellers are seeking a balance – they want to achieve financial goals while also feeling confident that they’ve made the right decision for all stakeholders involved, including clients, employees, and the community. The ideal outcome for many is a sense of accomplishment and peace of mind as they transition to the next phase of their professional or personal lives.

CONTENT

How important is it for the buyer of an insurance agency to be someone local?

The importance of a buyer being from the same city as the independent insurance agency being sold can vary depending on several factors.

Let’s explore this topic in more depth:

Local Market Knowledge and Relationships

A local buyer has several distinct advantages in understanding the specific market dynamics, local community needs and driving factors in the local economy. They have likely already established relationships with local businesses, community leaders, and potential clients. This familiarity can be beneficial for maintaining and growing the agency’s client base.

However, a non-local buyer with a strong track record of successful acquisitions in different markets might bring fresh perspectives and innovative approaches to benefit the agency.

Community Involvement and Reputation

Local buyers often have a vested interest in maintaining the agency’s community involvement and local reputation. They may be more likely to continue supporting local causes and maintaining the agency’s role in the community, as well as continuing any advertising or outreach programs your agency may have sponsored.

On the other hand, a non-local buyer might bring new resources and ideas for community engagement, potentially expanding the agency’s impact.

Employee and Client Retention

Local buyers might have an easier time retaining employees and clients due to their understanding of local culture and business practices. This can lead to a smoother transition and less disruption to the agency’s operations.

However, a non-local buyer with strong operational processes and a commitment to understanding and adapting to local needs can also succeed in retaining employees and clients.

Growth Opportunities

A local buyer might see immediate synergies with their existing business in the area, leading to quick growth opportunities. They may also have a better understanding of untapped local markets.

Conversely, a non-local buyer might bring access to new markets, carriers, or technologies that could significantly expand the agency’s reach and capabilities.

Long-Term Commitment

There’s often a perception that local buyers will have a stronger long-term commitment to the agency and the community. This can be reassuring for sellers who are concerned about their legacy.

However, many non-local buyers, especially those looking to expand into new markets, may have an equally strong commitment to the agency’s long-term success.

Operational Changes

Local buyers might be more inclined to maintain the agency’s current operational structure and culture, which can be appealing if the agency is already successful.

Non-local buyers might implement more significant changes, improving efficiency and profitability or disrupting established processes.

Negotiation and Valuation

Local buyers might have a better understanding of the local market value of the agency. However, this could work both ways – they might offer a lower price based on local comparisons, or they might be willing to pay a premium for a well-established local competitor.

Non-local buyers might base their valuation on broader market trends or strategic value, potentially leading to a different (higher or lower) valuation.

In conclusion, while there can be advantages to selling to a local buyer, it’s not necessarily a critical factor in the success of the sale or the agency’s future. The most important considerations should be the buyer’s overall fit with the agency’s values, their financial capability, their vision for the agency’s future, and their ability to serve clients effectively.

The decision should be based on a comprehensive evaluation of all potential buyers, considering factors such as their financial strength, operational capabilities, cultural fit, and plans for the agency’s future. Whether local or not, the ideal buyer is one who can provide the best overall outcome for the agency, its employees, its clients, and the selling owner.

CONTENT

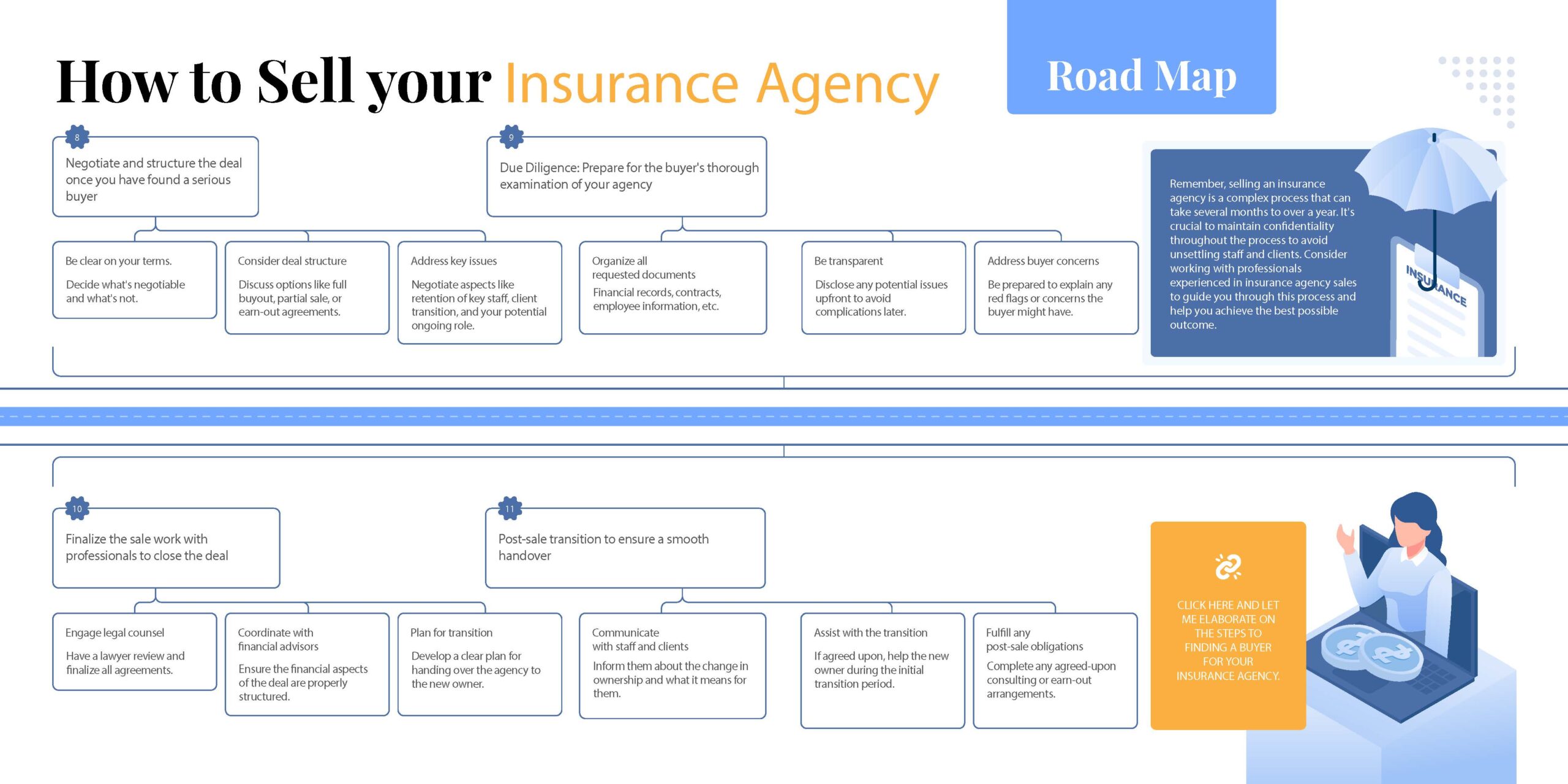

I want to sell my insurance agency.

What steps do I take to find a buyer for my business?

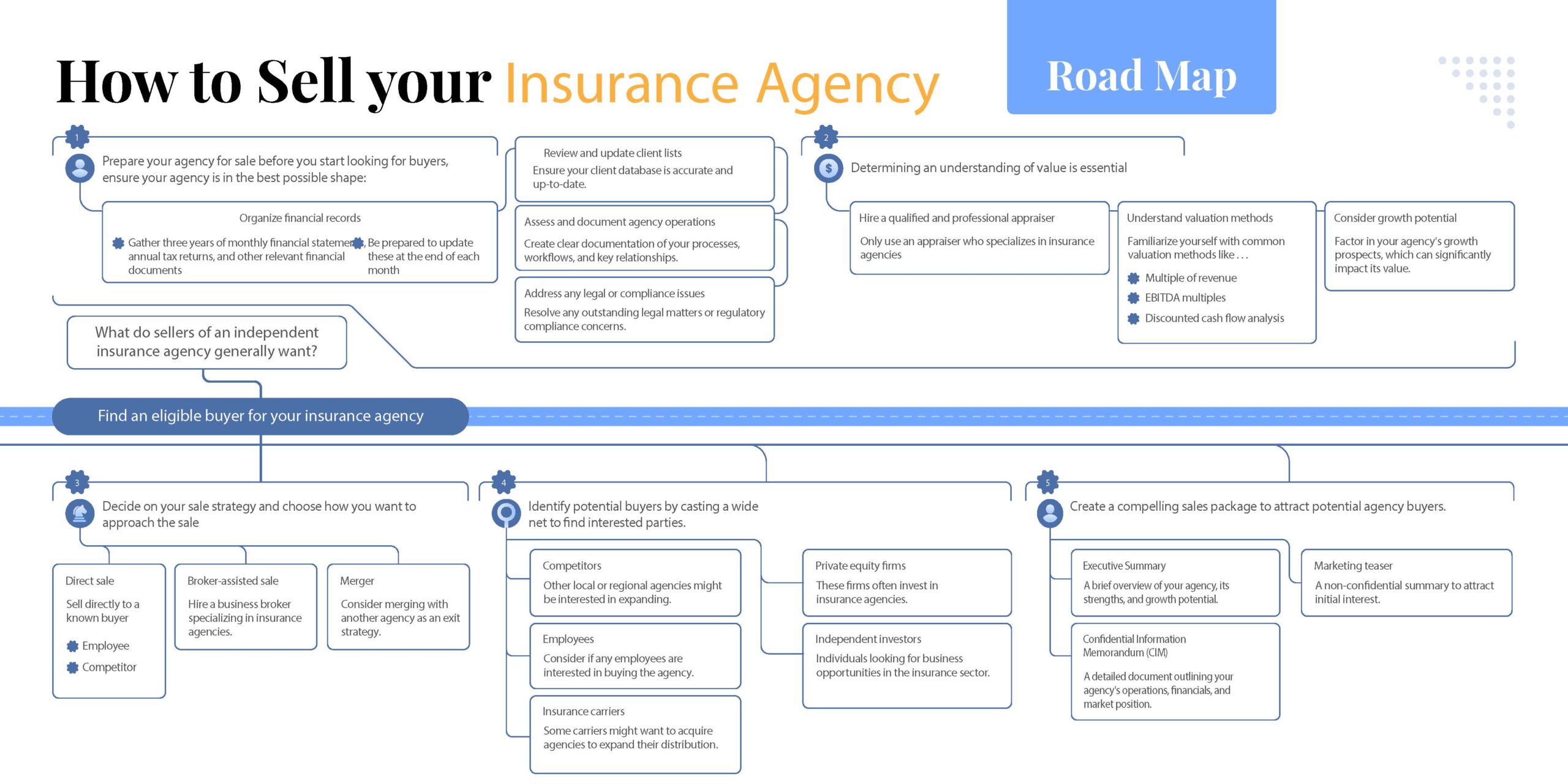

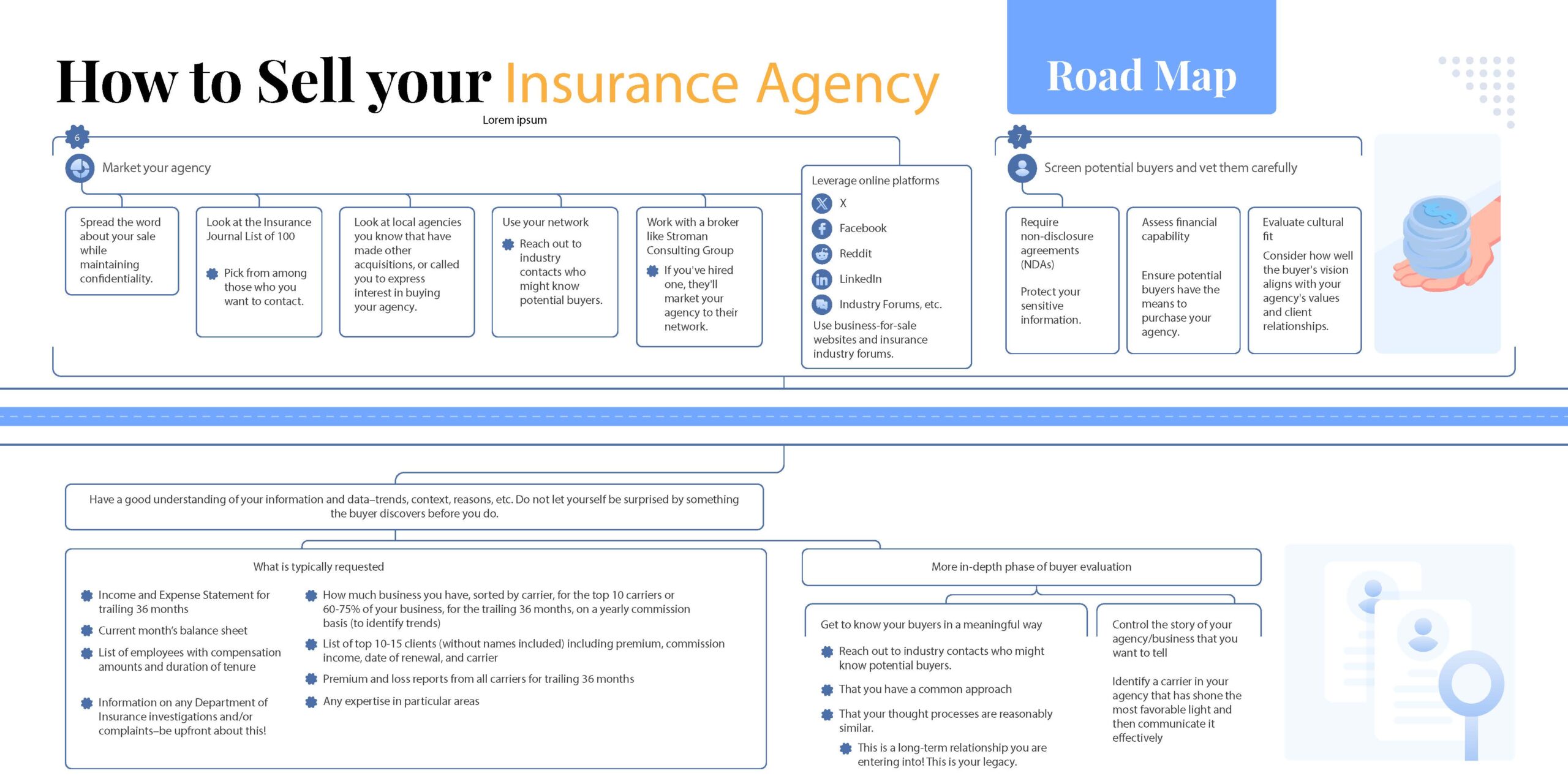

Selling an insurance agency is a significant decision that requires careful planning and execution. The process involves multiple steps, from preparing your agency for sale to transitioning ownership after closing the deal. This guide outlines the key stages involved in finding a buyer for your insurance agency, ensuring you’re well-equipped to navigate this complex journey. By following these steps, you can maximize the value of your agency and find a buyer who will continue your legacy of service to clients.

Selling your insurance agency is a complex process that requires careful planning, execution, and patience. By following these steps – from thorough preparation and accurate valuation to effective marketing and skilled negotiation – you can maximize your agency’s value and find the right buyer.

Remember to maintain confidentiality throughout the process and don’t hesitate to seek professional assistance from brokers, appraisers, lawyers, and financial advisors. With the right approach, you can successfully transition your agency to new ownership, ensuring continuity for your clients and staff while achieving your personal and financial goals. The journey will be challenging and very time-consuming, but with proper planning and execution, you can navigate the sale process successfully and move confidently into your next chapter in life.